Key Information Documents (KID)

Overview:

IBKR is required to provide EEA and UK retail customers with Key Information Documents (KID) for certain financial instruments.

Relevant products include ETFs, Futures, Options, Warrants, Structured Products, CFDs and other OTC products. Funds include both UCITS and non-UCITS funds available to retail investors.

Generally KIDs must be provided in an official language of the country in which a client is resident.

However, clients of IBKR have agreed to receive communications in English, and therefore if a KID is available in English all EEA and UK clients can trade the product regardless of their country of residence.

In cases where a KID is not available in English, IBKR additionally supports other languages as follows:

| Language | Can be traded by residents or citizens* of |

| German | Germany, Austria, Belgium, Luxembourg and Liechtenstein |

| French | France, Belgium and Luxembourg |

| Dutch | the Netherlands and Belgium |

| Italian | Italy |

| Spanish | Spain |

*regardless of country of residence

La fenêtre de compte TWS pour les clients de détail d'IBCE et IBIE

Overview:

Cet article décrit les informations fournies dans la fenêtre de compte de TWS pour les entités de l'Union européenne d'IBKR.

|

Les CFD sont des instruments complexes associés à un risque élevé de perte financière rapide en raison de l'effet de levier. 63,7 % des comptes d'investisseurs de détail perdent de l'argent lorsqu'ils tradent des CFD avec IBKR. Vous devez vous assurer que vous comprenez la manière dont fonctionnent les CFD et que vous pouvez vous permettre de courir un risque élevé de perte de capital. |

Background:

Les clients de détail résidents de l'EEE, qui détiennent un compte auprès d'un des courtiers européens d'IBKR, IBIE ou IBCE, sont soumis aux réglementations de l'Union européenne qui introduisent l'effet de levier et autres restrictions applicables aux transactions de CFD.

La réglementation exige l’utilisation de liquidités disponibles pour satisfaire aux exigences de marge CFD et interdit aux clients de détail d’utiliser des titres du compte comme garantie pour emprunter des fonds afin d’initier ou de maintenir une position CFD. Veuillez consulter l’Aperçu de la mise en œuvre des règles CFD de l’ESMA pour les clients de détail chez IBIE et IBCE pour plus de détails.

Les comptes des entités européennes d’IBKR sont des comptes universels dans lesquels les clients peuvent trader toutes les catégories d’actifs disponibles sur la plateforme IBKR, mais contrairement aux entités américaine et britannique d’IBKR, il n’y a pas de segments financés séparément.

Des exemples pratiques de la façon dont cette restriction est appliquée ainsi que des détails sur la façon dont les clients peuvent surveiller les liquidités disponibles pour les transactions CFD sont décrits ci-dessous.

Fenêtre de compte

IBKR applique la restriction relative aux liquidités disponibles en calculant les fonds disponibles pour le trading de CFD en temps réel, en rejetant les nouveaux ordres et en liquidant les positions existantes lorsque les liquidités disponibles sont insuffisantes pour couvrir les exigences de marge initiale et de maintien des CFD.

IBKR offre aux clients la possibilité de surveiller les liquidités disponibles pour les transactions de CFD via une amélioration de la fenêtre de compte TWS qui affiche le niveau de liquidités disponibles sur le compte. Il est important de noter que les fonds indiqués comme disponibles pour le trading de CFD n’impliquent pas que les liquidités soient détenues dans un segment distinct. Cela indique simplement la proportion du total des soldes de compte disponible pour le trading de CFD.

Par exemple, supposons qu'un compte ait 9 705 EUR de liquidités et pas de positions. La totalité des liquidités est disponible pour ouvrir des positions de CFD, ou des positions dans toute autre catégorie d'actifs :

Si le compte achète 10 actions d'AAPL pour une valeur totale de 1 383 USD, les espèces du compte seront

réduites par un montant correspondant en EUR, et les fonds disponibles pour le trading de CFD seront réduits du

même montant :

Veuillez noter que les fonds totaux disponibles sont réduits d’un montant inférieur, correspondant à l’exigence de marge d’action.

Si, au lieu d’acheter des actions AAPL, le compte achète 10 CFD AAPL, l’impact sera différent. Comme la transaction implique un contrat dérivé plutôt que l’achat de l’actif sous-jacent lui-même, il n’y a pas de réduction de trésorerie, mais les fonds disponibles pour les CFD sont réduits de l'exigence de marge CFD pour garantir la performance du contrat :

Dans ce cas, le total des fonds disponibles et les fonds disponibles pour CFD sont réduits d’un montant égal ; l’exigence de marge CFD.

Approvisionnement

Comme indiqué ci-dessus, les comptes basés au sein de l’UE n’ont pas de segments et il n’est donc pas nécessaire de procéder à des transferts internes. Les fonds sont disponibles pour les transactions dans toutes les catégories d’actifs dans les montants indiqués dans la fenêtre de compte, sans avoir besoin de sweeps ou de transferts.

Veuillez également noter que si un compte a un prêt sur marge, c’est-à-dire des liquidités négatives, il ne sera pas possible d’ouvrir des positions CFD car l’exigence de marge CFD doit être satisfaite par des liquidités disponibles et positives. Si vous avez un prêt sur marge et souhaitez trader des CFD, vous devez d’abord clôturer des positions de marge pour éliminer le prêt, ou ajouter des liquidités au compte d’un montant qui couvre le prêt sur marge et crée une réserve de liquidités suffisante pour la marge CFD nécessaire.

Présentation de la mise en place des règles ESMA concernant les CFD pour les clients de détail chez IBIE et IBCE

Overview:

|

Les CFD sont des instruments complexes associés à un risque élevé de perte financière rapide en raison de l'effet de levier. 69,4 % des comptes d'investisseurs de détail perdent de l'argent lorsqu'ils tradent des CFD avec IBKR. Vous devez vous assurer que vous comprenez la manière dont fonctionnent les CFD et que vous pouvez vous permettre de courir un risque élevé de perdre de l'argent. |

L'Autorité européenne des marchés financiers (ESMA) a adopté de nouvelles règles applicables aux clients de détail qui tradent des CFD, à compter du 1 août 2018. Les clients professionnels ne sont pas affectés.

Les régulateurs nationaux ont adoptés les règles ESMA de façon permanente.

Les règles consistent en: 1) des limites sur les effets de levier; 2) une règle de clôture des positions ouvertes par compte basée sur la marge 3) une protection contre les soldes négatifs par compte; 4) une restriction des incitations au trading de CFD; et 5) un avertissement standardisé concernant les risques.

La plupart des clients (à l'exception des entités régulées) sont initialement classés comme des clients de détail. IBKE peut, dans certaines circonstances accepter de changer la classification d'un client de détail en client professionnel ou un client professionnel en client de détail. Veuillez consulter la classification MiFID pour plus d'informations.

Les sections suivantes expliquent la manière dont IBKR (UK) a appliqué les mesures de l'ESMA.

1 Limites applicables aux effets de levier

1.1 Marge ESMA

Les limites applicables aux effets de levier fixées par l'ESMA à différents niveaux dépendent du sous-jacent :

- 3,33 % pour les paires de devises majeures; les paires de devises majeures sont une combinaison d'USD ; CAD ; EUR ; GBP ; CHF ; JPY

- 5 % pour les paires de devises non majeures et indices majeurs;

- Les paires de devises non majeures sont celles comprenant une devise qui n'est pas listée ci-dessus, ex. : USD.CNH

- Les indices principaux sont IBUS500, IBUS30, IBUST100, IBGB100, IBDE40, IBEU50, IBFR40, IBJP225, IBAU200

- 10 % pour les indices sur titres secondaires : IBES35, IBCH20, IBNL25, IBHK50

- 20 % pour les titres individuels

1.2 Marges appliquées - Exigence standard

En plus des marges de l'ESMA, IBKR établit ses propres exigences de marges (Marges IB) basées sur la volatilité historique du sous-jacent et autres facteurs. Nous appliquerons les marges IB si elles sont supérieures à celles déterminées par l'ESMA.

Vous trouverez des informations concernant les marges IB et ESMA applicables ici.

1.2.1 Marges appliquées - Marge minimum de concentration

Des frais de concentration sont appliqués si le portefeuille est composé d'un petit nombre de positions CFD et/ou actions, ou si les deux positions les plus importantes dominent. Nous soumettons le portefeuille à un test de résistance en appliquant un mouvement défavorable de 30 % sur les deux positions les plus importantes et un mouvement défavorable de 5 % sur les positions restantes. La perte totale obtenue sera alors utilisée comme exigence de marge de maintien si elle est supérieure à l'exigence standard pour les positions groupées d'actions et de CFD. Veuillez noter que les frais de concentration sont le seul cas où la marge des positions d'actions et de CFD est calculée ensemble.

1.3 Approvisionnement des exigences de marge initiale

Pour ouvrir une position de CFD, la marge initiale doit correspondre à celle de la trésorerie.

Initialement, toute la liquidité utilisée pour approvisionner le compte est disponible pour le trading de CFD. Toute exigence de marge initiale pour d’autres instruments et les liquidités utilisées pour acheter des actions en espèces réduisent les liquidités disponibles. Si vos achats d’actions au comptant ont créé un prêt sur marge, aucun fonds n’est disponible pour les transactions sur CFD, même si votre compte dispose de fonds propres importants. Nous ne pouvons pas augmenter un prêt sur marge pour approvisionner la marge de CFD, conformément aux règles ESMA.

Les profits réalisés pour les CFD sont inclus dans la trésorerie et disponibles immédiatement; la trésorerie ne doit pas nécessairement faire d'abord l'objet d'un règlement. Les profits non réalisés ne peuvent cependant pas être utilisés pour satisfaire les exigences de marge initiales.

2 Règle de clôture des positions ouvertes basée sur la marge

2.1 Calculs de la marge de maintien et liquidations

L'ESMA exige qu'IBKR liquide les positions de CFD lorsque la valeur de compte éligible devient inférieure à 50 % de la marge initiale requise pour ouvrir les positions. IBKR peut clôturer des positions plus tôt si notre analyse des risques est plus prudente. La valeur de compte éligible comprend la trésorerie de CFD et le P&L de CFD non réalisé (positif et négatif). Notez que les liquidités CFD excluent les liquidités à l'appui des exigences de marge pour d'autres instruments.

La base pour ce calcul est la marge initiale requise au moment de l'ouverture d'une position CFD. En d'autres termes, contrairement aux calculs de marge applicables aux positions autres que CFD, le montant de la marge initiale ne change pas lorsque la valeur de la position ouverte change.

2.1.1 Exemple

Vous avez 2000 EUR en espèces dans votre compte et pas de position ouverte. Vous souhaitez acheter 100 CFD de XYZ au prix limite de 100 EUR. 50 CFD sont d'abord exécutés, puis les 50 restants. Votre trésorerie disponible diminue au fur et à mesure des exécutions:

|

|

Trésorerie |

Valeur de compte* |

Position |

Prix |

Valeur |

P&L non réalisé |

MI |

MM |

Trésorerie disponible |

Violation MM |

|

Pré-trade |

2000 |

2000 |

|

|

|

|

|

|

2000 |

|

|

Post-trade 1 |

2000 |

2000 |

50 |

100 |

5000 |

0 |

1000 |

500 |

1000 |

Non |

|

Post-trade 2 |

2000 |

2000 |

100 |

100 |

10 000 |

0 |

2000 |

1000 |

0 |

Non |

*La valeur de compte est la trésorerie plus le P&L non réalisé

Le prix passe à 110. Votre valeur de compte est maintenant de 3000 mais vous ne pouvez pas ouvrir de positions supplémentaires car la trésorerie disponible est toujours de 0, et en vertu des règles de l'ESMA, les marges initiales (MI) et de maintien (MM) restent inchangées:

|

|

Trésorerie |

Titres |

Position |

Prix |

Valeur |

P&L non réalisé |

MI |

MM |

Trésorerie disponible |

MM Violation |

|

Variation |

2000 |

3000 |

100 |

110 |

11 000 |

1000 |

2000 |

1000 |

0 |

Non |

Puis le prix baisse et passe à 95. Votre valeur de compte passe à 1500 mais il n'y a pas de violation de marge puisque elle est toujours supérieure à l'exigence fixée à 1000 :

|

|

Trésorerie |

Titres |

Position |

Prix |

Valeur |

P&L non réalisé |

MI |

MM |

Trésorerie disponible |

Violation MM |

|

Variation |

2000 |

1500 |

100 |

95 |

9500 |

(500) |

2000 |

1000 |

0 |

Non |

Le prix baisse encore et passe à 85 ce qui se traduit par une violation de la marge et déclenche une liquidation :

|

|

Trésorerie |

Titres |

Position |

Prix |

Valeur |

P&L non réalisé |

MI |

MM |

Trésorerie disponible |

Violation MM |

|

Variation |

2000 |

500 |

100 |

85 |

8500 |

(1500) |

2000 |

1000 |

0 |

Oui |

3 Protection contre les valeurs négatives

Suite aux mesures de l'ESMA, votre responsabilité sur les CFD se limite aux fonds dédiés au trading de CFD. Les autres instruments financiers (ex. actions ou contrats à terme) ne peuvent pas être liquidés pour satisfaire une insuffisance de marge sur un CFD.*

Par conséquent, les actifs autres que les CFD ne font pas partie de votre capital sous risque pour le trading de CFD.

Si vous perdez plus que les fonds dédiés au trading de CFD, IB devra annuler la perte.

Étant donné que la protection contre les valeurs négatives représente un risque supplémentaire pour IBKR, nous facturerons aux investisseurs de détail un spread supplémentaire de 1 % pour les positions de CFD détenues d'une séance à l'autre. Vous trouverez le détail des taux de financement des CFD ici.

*Bien que nous ne puissions pas liquider les positions autres que CFD pour couvrir un déficit de CFD, nous pouvons liquider des positions de CFD pour couvrir un déficit non CFD.

TWS Account Window for Retail Clients of IBKR Ireland and Central Europe

Overview:

This article describes the information provided in the TWS account window for IBKRs EU based entities.

|

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 61% of retail investor accounts lose money when trading CFDs with IBKR. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. |

Background:

Retail clients who are residents of the EEA and therefore maintain an account with one of IBKR’s European brokers, IBIE or IBCE, are subject to EU regulations which introduce leverage and other restrictions applicable to CFD transactions.

Notably the regulations require the use of free cash to satisfy CFD margin requirements and prohibit retail clients from using securities in the account as collateral to borrow funds to initiate or maintain a CFD position. Please see Overview of ESMA CFD Rules Implementation for Retail Clients at IBIE and IBCE for full details.

The accounts of IBKRs EU entities are universal accounts in which clients can trade all asset classes available on IBKRs platform, but unlike IBKRs US and UK entities, there are no separately funded segments.

Working examples of how this restriction is applied, along with details as to how clients can monitor free cash available for CFD transactions, are outlined below.

Account Window

IBKR enforces the restriction relating to free cash by calculating the funds available for CFD trading on a real-time basis, rejecting new orders and liquidating existing positions when the available free cash is insufficient to cover CFD initial and maintenance margin requirements.

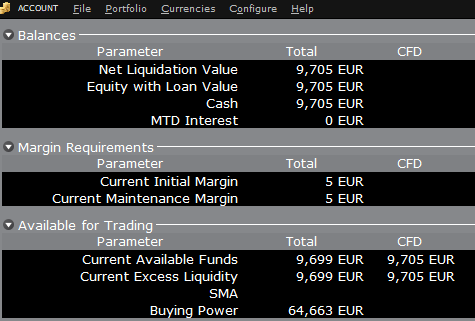

IBKR offers clients the ability to monitor free cash available for CFD transactions via an enhancement to the TWS Account Window which displays the level of free cash in the account. Importantly, the funds shown as available for CFD trading do not imply that cash is held in a separate segment. It simply indicates what proportion of total account balances is available for CFD trading.

For example, assume that an account has EUR 9,705 in cash and no positions. All the cash is available to open CFD positions, or positions in any other asset class:

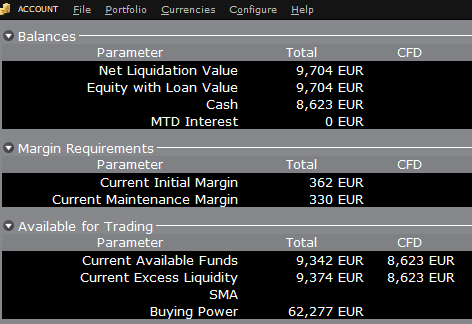

If the account now purchases 10 shares of AAPL stock for an aggregate value of USD 1,383 the cash in the account is reduced by a corresponding amount in EUR, and the funds available for CFD trading are reduced by the

same amount:

Note that Total available funds are reduced by a smaller amount, corresponding to the stock margin requirement.

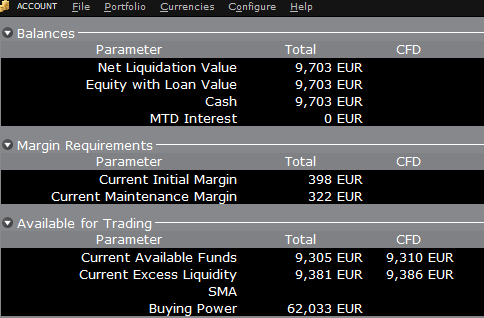

If, instead of buying AAPL stock, the account buys 10 AAPL CFDs the impact will be different. As the transaction involves a derivative contract rather than the purchase of the underlying asset itself, there’s no reduction in cash but the funds available for CFDs are reduced by the CFD margin requirement to secure performance on the contract:

In this case Total available funds and CFD available funds are reduced by an equal amount; the CFD margin requirement.

Funding

As noted above, EU-based accounts do not have segments and therefore there is no need for internal transfers. Funds are available for trades in all asset classes in the amounts indicated in the account window, without the need for sweeps or transfers.

Note also that should an account have a margin loan, i.e. negative cash, it will not be possible to open CFD positions since the CFD margin requirement must be satisfied by free, positive cash. Should you have a margin loan and wish to trade CFDs you must first either close margin positions to eliminate the loan, or add cash to the account in an amount that covers the margin loan and creates a cash buffer sufficient for the necessary CFD margin.

IBKR Metals CFDs – Facts and Q&A

Overview:

The following article is intended to provide a general introduction to London Gold and Silver Contracts for Differences (CFDs) issued by IBKR.

Please follow these links for information on IBKR Share CFDs, Index CFDs and Forex CFDs.

Risk Warning

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

61% of retail investor accounts lose money when trading CFDs with IBKR.

You should consider whether you understand how CFDs work and whether you can afford to take the

high risk of losing your money.

ESMA Rules for CFDs (Retail Clients only)

The European Securities and Markets Authority (ESMA) has enacted new CFD rules effective 1st August

2018.

The rules include: 1) leverage limits on the opening of a CFD position; 2) a margin close out rule on a per

account basis; and 3) negative balance protection on a per account basis.

The ESMA Decision is only applicable to retail clients. Professional clients are unaffected.

Please refer to the following articles for more detail:

ESMA CFD Rules Implementation at IBKR (UK) and IBKR LLC

ESMA CFD Rules Implementation at IBIE and IBCE

Introduction

A London Gold CFD enables you to have exposure to price movements of physical Gold without actually owning it. A London Gold CFD is an agreement between you and IBKR to exchange the difference in price of the underlying over a period of time. The difference to be exchanged is determined by the change in the reference price of the underlying. Thus, if the price of physical Gold traded on the London bullion market rises and you are long the CFD, you receive cash from IBKR and vice versa. A London Gold CFD can be bought long or sold short to suit your view of market direction in the future.

Contract Specifications

| Contract | IBKR Symbol | Per Trade Fee | Minimum per Order | Multiplier |

| London Gold | XAUUSD | 0.015% | USD 2.00 | 1 |

| London Silver | XAGUSD | 0.03% | USD 2.00 | 1 |

Price Determination

The IBKR London Gold and Silver CFDs reference physical Gold and Silver traded on the London bullion market. The London bullion market is a wholesale over-the-counter market for the trading of precious metals. Trading is conducted among members of the London Bullion Market Association (LBMA). Most of the members are major international banks.

IBKR receives quote streams from approximately 10 such major banks, in much the same way it does for cash forex. IBKR Smart routes between the banks, and the best available price at any given time becomes the reference price for the CFDs. IBKR does not add a spread to the banks’ quotes.

Low Commissions and Financing Rates: Unlike other CFD providers IBKR charges a transparent

commission, rather than widening the spread. Commission rates are only 0.015% for London Gold and 0.03% for London Silver. Overnight financing rates are just benchmark +/- 1.5% (an additional 1% surcharge is added for retail accounts).

Transparent Quotes: Because IBKR does not widen the spread, the Metals CFD quotes accurately

represent the spreads and price movements of the related cash metal, as described above.

Margin Efficiency: IBKR establishes house-margin requirements based on historic volatility of the

underlying and other factors. Retail clients are subject to regulatory minimum initial margins of 5% for

London Gold or 10% for London Silver.

Trading Permissions: Same as for Share and Index CFDs.

Market Data Permissions: Metals CFD market data is free, but a permission is required for system

reasons.

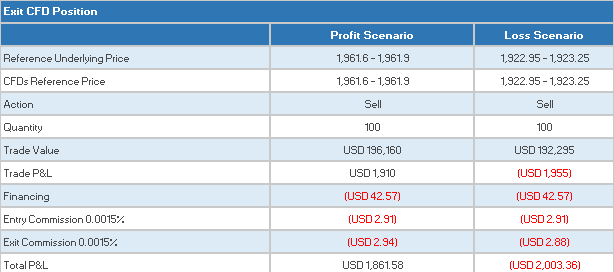

Worked Trade Example (Professional Clients):

You purchase 100 XAUUSD CFDs at $1,942.5 for USD 194,250 which you then hold for 5 days.

![]()

Closing the Position

CFD Resources

Below are some useful links with more detailed information on IB’s CFD offering:

Frequently asked Questions

Are short Metals CFDs subject to forced buy-in?

No.

Can I take delivery of the underlying metal?

No, IBKR does not support physical delivery for Metals CFDs.

Are there any market data requirements?

The market data for Metal CFDs is free, and is included the market data for Index CFDs. However, you need to subscribe to the permission for system reasons. To do this, log into Account Management, and click through the following tabs: Settings/User Settings/Trading Platform/Market Data Subscriptions. Alternatively you can set up an Index or Metals CFD in your TWS quote monitor and click the “Market Data Subscription Manager” button that appears on the quote line.

How are my CFD trades and positions reflected in my statements?

If you are a client of IBKR (U.K.) or IBKR LLC, your CFD positions are held in a separate account segment identified by your primary account number with the suffix “F”. You can choose to view Activity Statements for the F-segment either separately or consolidated with your main account. You can make the choice in the statement window in Account Management.

If you are a client of other IBKR entities, there is no separate segment. You can view your positions normally alongside your non-CFD positions.

In what type of IB accounts can I trade CFDs e.g., Individual, Friends and Family,

Institutional, etc.?

All margin and cash accounts are eligible for CFD trading.

Can I trade CFDs over the phone?

No. In exceptional cases we may agree to process closing orders over the phone, but never opening

orders.

Can anyone trade IB CFDs?

All clients can trade IB CFDs, except residents of the USA, Canada, Hong Kong, New Zealand and

Israel. There are no exemptions based on investor type to the residency-based exclusions.

Bonus Certificates Tutorial

Introduction

Bonus certificates are designed to provide a predictable return in sideways markets, and market returns in rising markets.

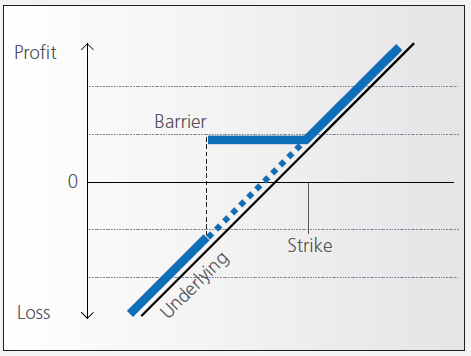

At the time they’re issued, bonus certificates normally have a term to maturity of two to four years. You will receive a specified cash pay-out (“bonus level” or “Strike”) if at maturity the price of the underlying is below or at the strike, as long as the underlying instrument has not touched or fallen below an established price level (“safety threshold” or “barrier”) during the term of the certificate.

Unless the certificate has a cap, you continue to participate in the price gains if the underlying instrument rises above the bonus level. In this case you either receive the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

However, if the barrier is breached, you will no longer be entitled to the bonus payment. The value of the certificate then corresponds to the value of the underlying (times the ratio). In other words, once the barrier has been touched the certificate effectively converts to an index certificate. You will receive either the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

Although there is no structured leverage, the presence of the barrier creates effective leverage. When the price of the underlying instrument approaches the barrier the probability of a breach increases, affecting the price of the certificate disproportionately.

Pay-out Profile

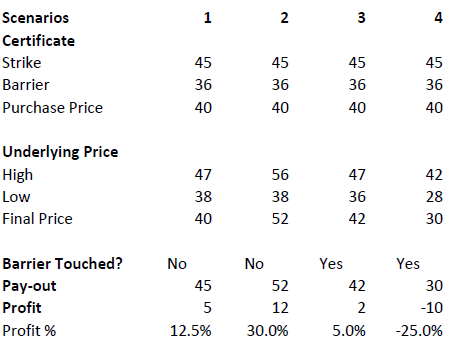

Example

Assume a bonus certificate on ABC share. The certificate has a strike of EUR 45.00 and a barrier set at EUR 36.00. The table below shows scenarios depending on the trading range of the underlying, the final price of the underlying and whether the barrier has been touched or not.

Warrant Tutorial

Introduction

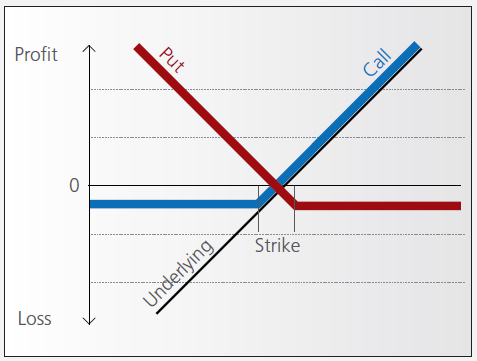

A warrant confers the right to buy (call-warrant) or sell (put-warrant) a specific quantity of a specific underlying instrument at a specific price over a specific period of time.

Pay-out Profile

With some warrants, the option right can only be exercised on the expiration date. These are referred to as “European-style” warrants. With “American-style” warrants, the option right can be exercised at any time prior to expiration. The vast majority of listed warrants are cash-exercised, meaning that you cannot exercise the warrant to obtain the underlying physical share. The exception to this rule is Switzerland, where physically settled warrants are widely available.

IBKR does allow for US and Canadian warrant exercise. Customers wishing to do so should submit a Customer Service ticket stating the name/symbol of the warrant, the quantity of shares and the intended action (i.e. exercise). The broker will pass through all associated exercise costs to the customer upon completion of the request. US or Canadian warrants are not eligible for auto-exercise at expiration. Warrants remaining in an account at expiration will be removed as worthless.

Factors that influence pricing

Not only do changes in the price of the underlying instrument influence the value of a warrant, a number of other factors are also involved. Of particular importance to investors in this regard are changes in volatility, i.e. the degree to which the price of the underlying instrument fluctuates. In addition, changes in interest rates and the anticipated dividend payments on the underlying instrument also play a role.

However, changes in implied volatility - as well as interest rates and dividends - only affect the time value of a warrant. The primary driver - intrinsic value - is solely determined by the difference between the price of the underlying instrument and the specified exercise price.

Historical and implied volatility

In addressing this topic, a differentiation has to be made between historical and implied volatility. Implied volatility reflects the volatility market participants expect to see in the financial instrument in the days and months ahead. If implied volatility for the underlying instrument increases, so does the price of the warrant.

This is because the probability of profiting from a warrant during a particular time-frame increases if the price of the underlying instrument is highly volatile. The warrant is therefore more valuable.

Conversely, if implied volatility decreases, that leads to a decline in the value of warrants and hence occasionally to nasty surprises for warrant investors who aren’t familiar with the concept and influence of volatility.

Interest rates and dividends

Issuers hedge themselves against price changes in the warrant through purchases and sales of the underlying instrument. Due to the leverage afforded by warrants, the issuer needs considerably more capital to hedge its exposure than you require to buy the warrants. The issuer’s interest expense associated with that capital is included in the price of the warrant. The amount of embedded interest reduces over time and at expiration is zero.

In the case of puts, the situation is exactly the opposite. Here, the issuer sells the underlying instrument

short to establish the necessary hedge, and in so doing receives capital that can earn interest. Thus interest reduces the price of the warrant by an amount that decreases over time.

As the issuer owns shares as a part of its hedging operations, it is entitled to receive the related dividend

payments. That additional income reduces the price of call warrants and increases the price for puts. But if the dividend expectations change, that will have an influence on the price of the warrants. Unanticipated special dividends on the underlying instrument can lead to a price decline in the related warrants.

Key valuation factors

Let’s assume the following warrant:

Warrant Type: Call

Term to expiration: 2 years

Underlying : ABC Share

Share price: EUR 30.00

Strike: EUR 30.00

Exercise ratio: 0.1

Warrant’s price: EUR 0.30

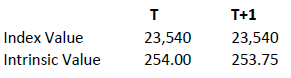

Intrinsic value

Intrinsic value represents the amount you could receive if you exercised the warrant immediately and then bought (in the case of a call) or sold (put) the underlying instrument in the open market.

It’s very easy to calculate the intrinsic value of a warrant. In our example the intrinsic value is EUR 00.00

and is calculated as follows:

(price of underlying instrument – strike price) x exercise ratio

= (EUR 30.00 – EUR 30.00) x 0.1

= EUR 00.00

If the price of the ABC share increases by EUR 1, the intrinsic value becomes

= (EUR 31.00 – EUR 30.00) x 0.1

= EUR 00.10

The intrinsic value of a put warrant is calculated with this formula:

(strike price – price of underlying instrument) x exercise ratio

It’s important to note that the intrinsic value of a warrant can never be negative. By way of explanation:

if the price of the underlying instrument is at or below the exercise price, the intrinsic value of a call equals zero. In this instance, the price of the warrant consists only of “time value”. On the flipside, the intrinsic value of a put is equal to zero if the price of the underlying instrument is at or above the exercise price.

Time value

Once you’ve calculated the intrinsic value of a warrant, it’s also easy to figure out what the time value of that warrant is. You simply deduct the intrinsic value from the current market price of the warrant. In our example, the time value is equal to EUR 1.30 as you can see from the following calculation:

(warrant price – intrinsic value)

= (EUR 0.30 EUR – EUR 0.00)

= EUR 0.30

Time value gradually erodes during the term of a warrant and ultimately ends up at zero upon expiration. At that point, warrants with no intrinsic value expire worthless. Otherwise you can expect to receive payment of the intrinsic value. Take note, though: a warrant’s loss of time value accelerates during the final months of its term.

Premium

The premium indicates how much more expensive a purchase/sale of the underlying instrument would be via the purchase of a warrant and the immediate exercise of the option right as opposed to simply buying/selling the underlying instrument in the open market.

Hence the premium is a measure of how expensive a warrant actually is. It follows that, when given a choice between warrants with similar features, you should always buy the one with the lowest premium. By calculating the premium as an annualized percentage, warrants with different terms to expiry can be compared with each other.

The percentage premium for the call warrant in our example can be calculated as follows:

(strike price + warrant price / exercise ratio – share price) / share price * 100

= (EUR 30.00 + EUR 0.30 / 0.1 – EUR 30.00) / EUR 30.00 x 100

= 10 percent

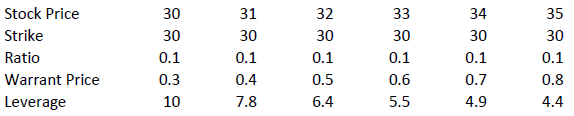

Leverage

The amount of leverage is the price of the share * ratio divided by the price of the warrant. In our example 30.00*0.1/0.3 = 10. So when the price of ABC increases by 1% the value of the warrant increases by 10%.

The amount of leverage is not constant however; it varies as intrinsic and time value changes, and is particularly sensitive to changes in intrinsic value. As a rule of thumb, the higher the intrinsic value of the warrant, the lower the leverage. For example (assuming constant time value):

Knock-out (Turbo) Tutorial

Introduction

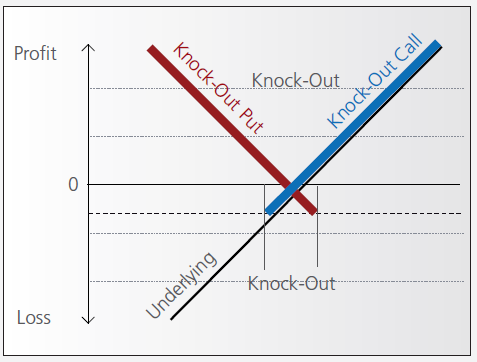

Knock-out warrants (turbos), like vanilla warrants, derive their value from the difference between the price of the underlying and the strike. They differ significantly however from vanilla warrants in many important respects:

- They can expire (knock-out) prematurely if the price of the underlying instrument touches or falls below (in the case of knock-out calls) or exceeds (in the case of knockout puts) a predetermined barrier-level. It expires worthless if the barrier equals the strike, or it may have a residual stop-loss value if the barrier is set higher than the strike (in the case of a call).

- Changes in implied volatility have little or no impact on knock-out products, therefore their pricing is easier for investors to comprehend than that of warrants.

- They have little or no time value (because of the presence of the knock-out barrier), and therefore have a higher degree of leverage than a warrant with the same strike. This is because the absence of time value makes the instrument “cheaper”.

Pay-out Profile

Leverage

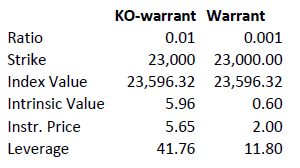

As discussed above, knock-out warrants exhibit high degrees of leverage, particularly as the price of the underlying nears the strike/barrier. Consider the following example of a long turbo on the Dow Jones Index, compared to a vanilla warrant:

Intrinsic value = (index value – strike) x ratio

Leverage = Index Value x Ratio / Instrument Price

A vanilla warrant retains significant time value even as the underlying price approaches the strike, sharply reducing its leverage compared to a knock-out warrant.

Product types

As discussed above, the barrier may either equal the strike, or be set above (calls) or below (puts). In the latter cases a small residual value remains after knock-out, corresponding to the difference between the barrier (the stop-loss level) and the strike.

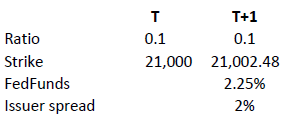

Moreover, knock-out products may either have an expiration date or may be open-ended. This makes a difference in the way interest is accounted for. If the contract has an expiration date interest is included in the premium, the amount of which reduces over time and is zero on expiration. This is analogous to a standard vanilla warrant.

in relation to an expiration date. The price of the contract therefore corresponds exactly to its intrinsic value. Interest however must be accounted for. This is done by a daily adjustment of the barrier and strike. The following example shows the daily adjustment for a long open-end turbo on the Dow Jones Index:

The adjustment = Strike T x (1+ FedFunds/360 + Issuer Spread/360).

The intrinsic value of the instrument is correspondingly reduced as follows, assuming no change in the value of the DJ Index):

Intrinsic value = (index value – strike) x ratio

Discount Certificates Tutorial

Introduction

Discount certificates are designed to provide an enhanced return in sideways markets, compared to a direct investment in the underlying.

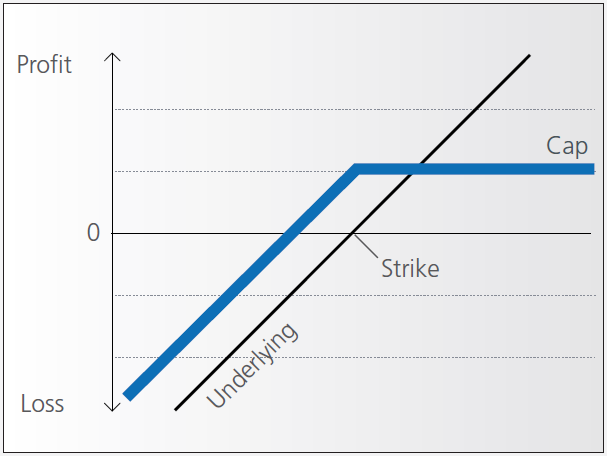

Discount certificates make it possible for you to buy an underlying instrument for less than its current market price. However, the maximum payback on a discount certificate is limited to a predetermined amount (cap).

Discount certificates normally have a term to maturity of one to three years. At maturity, a determination is made of where the price of the underlying instrument stands.

If it is at or above the cap, you’ll earn the maximum return and receive payment of the amount reflected by the cap.

If the price of the underlying instrument is below the cap on the maturity date, you’ll receive either the corresponding number of shares or a cash settlement reflecting the value of the underlying instrument on the maturity date.

Pay-out Profile

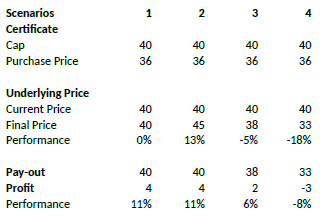

Example

Assume a discount certificate on ABC share. The certificate has a cap of EUR 40.00, and a purchase price of EUR 36.00. The table below shows scenarios depending on the final price of the underlying.

Factor Certificates Tutorial

Introduction

Factor certificates employ a daily leverage factor that multiplies the daily performance of the underlying instrument. Unlike knock-out warrants and mini-futures, factor certificates do not have a knock-out barrier. To avoid a loss greater than the investment, the calculation resets intraday if the performance of the underlying threatens to render the certificate worthless.

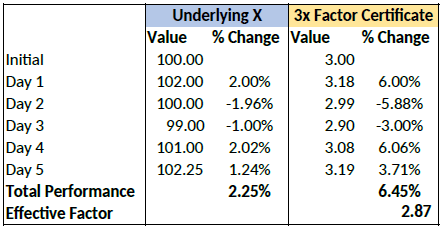

Daily Leverage

The performance of the certificate is calculated daily, without reference to previous days’ values. If the underlying returns 1% on the day, the value of 3x certificate increases by 3%, a 5x by 5%. The next day the process is repeated, referencing the prior day’s underlying close.

As such, factor certificates are particularly suitable for day-traders.

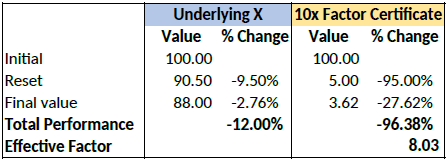

However, for a period of more than one day, the cumulative performance of the underlying cannot be simply multiplied by a factor of 3 as the previous day’s price always forms the new basis of calculating each day’s performance for the certificate. To illustrate with an example:

Cumulatively, the factor certificate has returned less than 3x the performance of the underlying.

Intraday Reset

If an underlying for a factor certificate loses more than a certain percentage of its value intraday, the calculation is reset by simulating a new day. The reset threshold varies depending on the leverage factor.

Let’s assume a long factor certificate with a 10x leverage factor. According to the terms of the certificate, a reset will be triggered if the underlying loses more than 9.5% during the calculation day.

Let’s now assume that the underlying loses 12% of its value during a particular day. The reset

and final performance will be as follows: